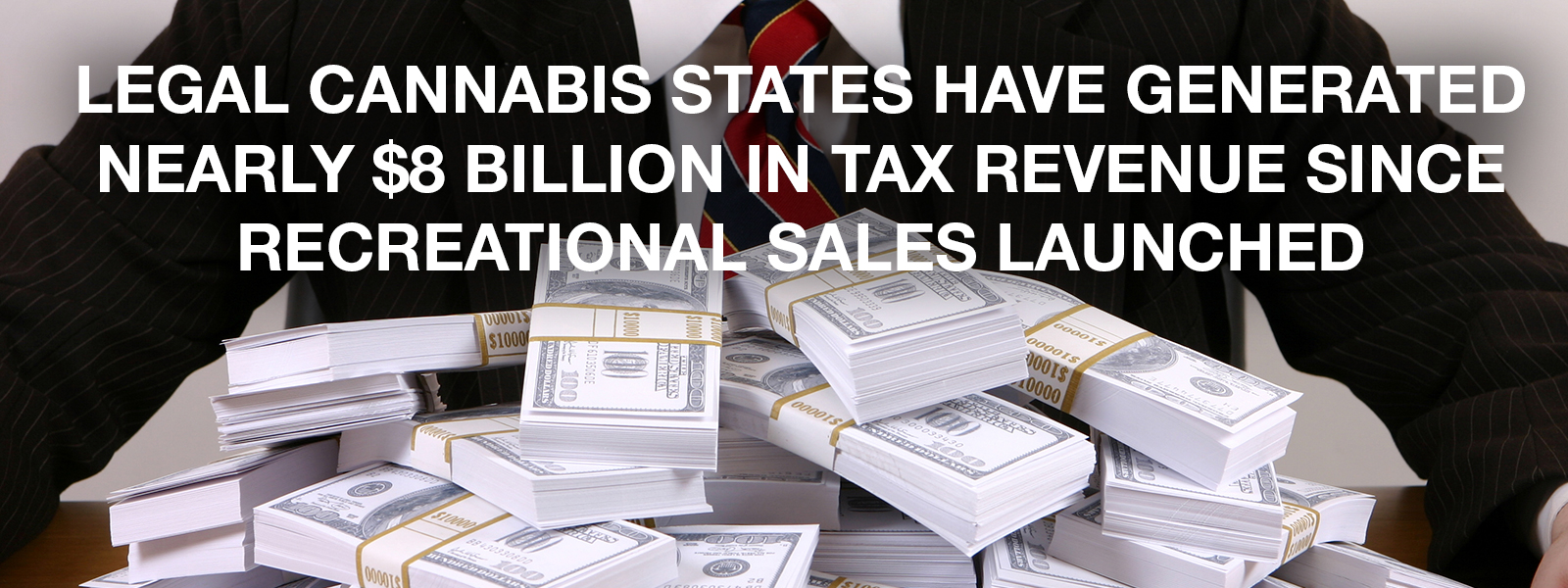

With A 55% Increase Over Last Year, Sales Of California Legal Adult-Use Cannabis Generated $817 Million In Tax Revenue

According to a report by the nonpartisan California Legislative Analyst’s Office, California collected about $817 million in adult-use marijuana tax revenue during the 2020-2021 fiscal year, state officials estimated on Monday. That’s 55% more cannabis earnings for state coffers than was generated in the prior fiscal year. Furthermore, the combined excise and cultivation tax revenue for the fourth quarter, which ended in June, amounted to $212 million—roughly tying the first quarter of the fiscal year for the most tax dollars raised in any single three-month period since legal sales launched.

This tremendous growth is further confirmed by the California Department of Tax and Fee Administration (“CDTFA”) which issued its analysis of the new data that since January 2018, total recreational marijuana revenue to date for the state is $2.8 billion, which includes $1.4 billion in excise tax, $347.4 million in cultivation tax and $1 billion in sales tax.

With about 37 states now legalizing some form of cannabis use, you would think that it is now time for the Federal government to change course.

The Anti-Federal U.S. Climate

The Federal Controlled Substances Act (“CSA”) 21 U.S.C. § 812 classifies marijuana as a Schedule 1 substance with a high potential for abuse, no currently accepted medical use in treatment, and lack of accepted safety for use under medical supervision. Although you can still face federal criminal charges for using, growing, or selling weed in a manner that is completely lawful under California law, the federal authorities in the past have pulled back from targeting individuals and businesses engaged in medical marijuana activities. This pull back came from Department of Justice (“DOJ”) Safe Harbor Guidelines issued in 2013 under what is known as the “Cole Memo”.

The Cole Memo included eight factors for prosecutors to look at in deciding whether to charge a medical marijuana business with violating the Federal law:

- Does the business allow minors to gain access to marijuana?

- Is revenue from the business funding criminal activities or gangs?

- Is the marijuana being diverted to other states?

- Is the legitimate medical marijuana business being used as a cover or pretext for the traffic of other drugs or other criminal enterprises?

- Are violence or firearms being used in the cultivation and distribution of marijuana?

- Does the business contribute to drugged driving or other adverse public health issues?

- Is marijuana being grown on public lands or in a way that jeopardizes the environment or public safety?

- Is marijuana being used on federal property?

Since 2013, these guidelines provided a level of certainty to the marijuana industry as to what point could you be crossing the line with the Federal government. But on January 4, 2018, then Attorney General Jeff Sessions revoked the Cole Memo. Now U.S. Attorneys in the local offices throughout the country retain broad prosecutorial discretion as to whether to prosecute cannabis businesses under federal law even though the state that these businesses operate in have legalized some form of marijuana.

Joyce-Blumenauer Amendment (previously referred to as the Rohrabacher-Farr Amendment)

Building on the DOJ’s issuance of the Cole Memo, in 2014 the House passed an amendment to the yearly federal appropriations bill that effectively shields medical marijuana businesses from federal prosecution. Proposed by Representatives Rohrabacher and Farr, the amendment forbids federal agencies to spend money on investigating and prosecuting medical marijuana-related activities in states where such activities are legal.

The amendment states that:

NONE OF THE FUNDS MADE AVAILABLE UNDER THIS ACT TO THE DEPARTMENT OF JUSTICE MAY BE USED, WITH RESPECT TO ANY OF THE STATES OF ALABAMA, ALASKA, ARIZONA, ARKANSAS, CALIFORNIA, COLORADO, CONNECTICUT, DELAWARE, FLORIDA, GEORGIA, HAWAII, ILLINOIS, INDIANA, IOWA, KENTUCKY, LOUISIANA, MAINE, MARYLAND, MASSACHUSETTS, MICHIGAN, MINNESOTA, MISSISSIPPI, MISSOURI, MONTANA, NEVADA, NEW HAMPSHIRE, NEW JERSEY, NEW MEXICO, NEW YORK, NORTH CAROLINA, NORTH DAKOTA, OHIO, OKLAHOMA, OREGON, PENNSYLVANIA, RHODE ISLAND, SOUTH CAROLINA, TENNESSEE, TEXAS, UTAH, VERMONT, VIRGINIA, WASHINGTON, WEST VIRGINIA, WISCONSIN, AND WYOMING, OR WITH RESPECT TO THE DISTRICT OF COLUMBIA, GUAM, OR PUERTO RICO, TO PREVENT ANY OF THEM FROM IMPLEMENTING THEIR OWN LAWS THAT AUTHORIZE THE USE, DISTRIBUTION, POSSESSION, OR CULTIVATION OF MEDICAL MARIJUANA.

This action by the House is not impacted by the change of position by the DOJ. However, unless this amendment gets included in each succeeding federal appropriations bill, the protection from Federal prosecution of medical marijuana businesses will no longer be in place. Fortunately, Congress has included this amendment but yet has changed any of the tax or banking laws that pose challenges to the cannabis industry.

Clearly, to avail yourself of the protections of the amendment, you must be on the medical cannabis side and you must be in complete compliance with your State’s medical cannabis laws and regulations. You may not be covered under the amendment if you are involved in the recreational cannabis side even if legal in the State you are operating.

What Should You Do?

Given the illegal status of cannabis under Federal law you need to protect yourself and your marijuana business from all challenges created by the U.S. government. Although cannabis is legal in California, that is not enough to protect you. Be proactive and engage an experienced Cannabis Tax Attorney in your area. Let the tax attorneys of the Law Offices Of Jeffrey B. Kahn, P.C. located in Orange County, Inland Empire (Ontario and Palm Springs) and other California locations protect you and maximize your net profits. And if you are involved in crypto currency, check out what a bitcoin tax attorney can do for you.

Follow

Follow Follow

Follow